Monday, October 30, 2006

Walmart and Semiconductors are signaling that Party is over

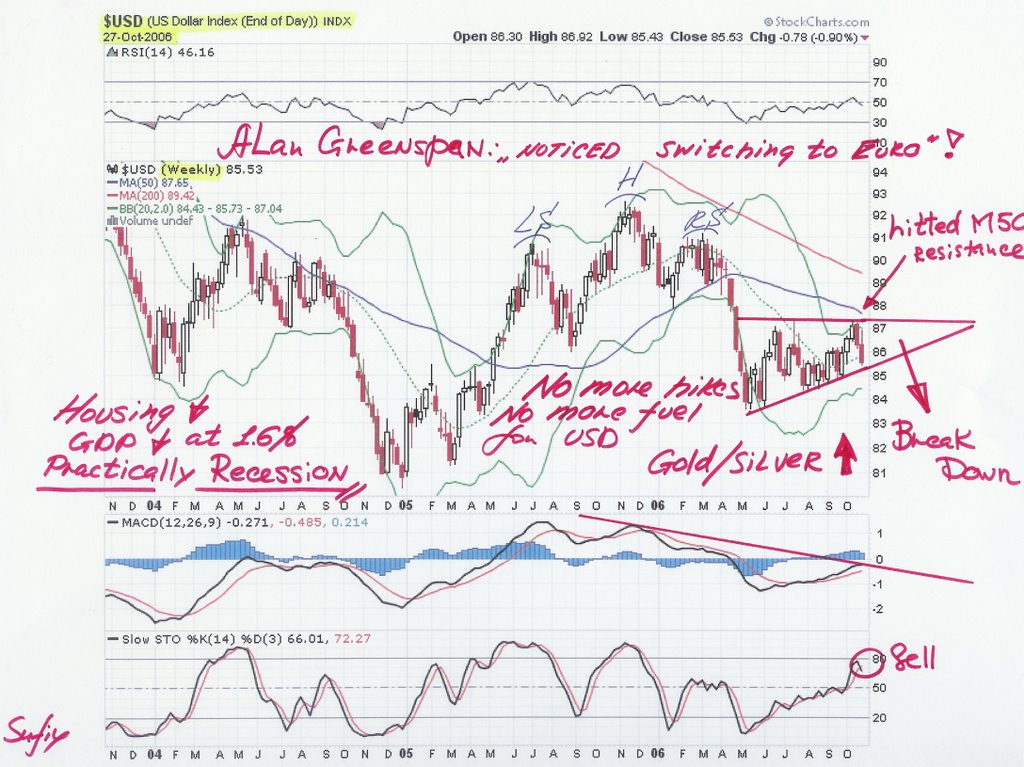

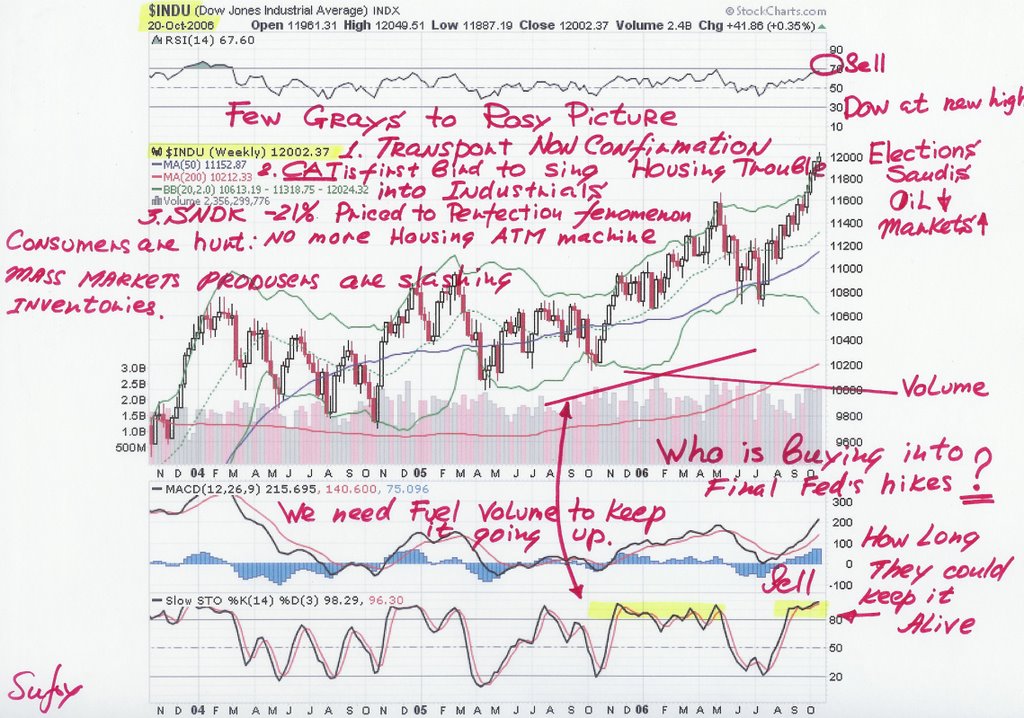

If you talk WMT you talk American consumer, if it can not grow Sales any more even with artificially low oil prices for Election Rally it tells real trouble: yield curve is inverted for reason - it is practically recession already. Transportation with Double Top signaled contraction earlier in Mid Year. And now story about SNDK is making its way into PC market and bellwether of Tech semiconductors will take the hit soon. Party is coming to The END check your Water Supply.

Tenke Mining Fireworks Has Begun

From previous post on Tenke Mining: "I wrote it after Western Silver acquisition: "The new deal in my opinion will be catalysis for much higher price valuations of Juniors with real resources. From Hommel: WTZ has metal resources in zinc, Silver, copper and lead at current prices worth of USD10 bio in the ground with PRODUCTION. Glamis is buying it for USD 1 bio 1 to 10 price/resource rate.

From Paradigm research: DRC alone account for 71.5 bio Cu eq lb*2.27USD/lb*24.75%=40.3USD bio Tenke's share rock value in the ground. In WTZ - Silver, but here we have all Argentina properties and Jose Maria bulk tonnage discovery (not included in this rock value)

With start of production in 2008 even if prices stay the same level TNK potentially MC is 4.0USD bio (without new major Argentina discoveries and increased reserves in DRC). They will have to finance 24.75% part of mine in DRC, I am not sure about the cost but if even we take dilution of 10 mio at CAD15.0 average it will bring 150 mio CAD for all activities. With FD at 51.7 mio plus dilution of 10 mio we will have in 2008 FD 61.7 SHARE PRICE TARGET CAD75.0

Now everybody can do DD and add potential Argentina, price rise in Cobalt and Copper, less dilution due to debt use.

Minus of course that it is DRC, but ... with time for mining it could be valued more than USA.

To unlock all this value we need couple of smart decisions of Lundins: spin off Argentina comes to mind, buy out TNR and on this base consolidation of all gold projects of Lundin group RBI, CGH - the new GOLD Co will move into new league right away: PRODUCER with big exploration potential with much higher valuation of gold properties.

Best luck to shareHOLDERS,

Sufiy."

First part has already happen PP for CAD103 mil at CAD12.70 bought out by Lundin family."

Regards,

Sufiy.

From Paradigm research: DRC alone account for 71.5 bio Cu eq lb*2.27USD/lb*24.75%=40.3USD bio Tenke's share rock value in the ground. In WTZ - Silver, but here we have all Argentina properties and Jose Maria bulk tonnage discovery (not included in this rock value)

With start of production in 2008 even if prices stay the same level TNK potentially MC is 4.0USD bio (without new major Argentina discoveries and increased reserves in DRC). They will have to finance 24.75% part of mine in DRC, I am not sure about the cost but if even we take dilution of 10 mio at CAD15.0 average it will bring 150 mio CAD for all activities. With FD at 51.7 mio plus dilution of 10 mio we will have in 2008 FD 61.7 SHARE PRICE TARGET CAD75.0

Now everybody can do DD and add potential Argentina, price rise in Cobalt and Copper, less dilution due to debt use.

Minus of course that it is DRC, but ... with time for mining it could be valued more than USA.

To unlock all this value we need couple of smart decisions of Lundins: spin off Argentina comes to mind, buy out TNR and on this base consolidation of all gold projects of Lundin group RBI, CGH - the new GOLD Co will move into new league right away: PRODUCER with big exploration potential with much higher valuation of gold properties.

Best luck to shareHOLDERS,

Sufiy."

First part has already happen PP for CAD103 mil at CAD12.70 bought out by Lundin family."

Regards,

Sufiy.

Sunday, October 29, 2006

Tuesday, October 24, 2006

How many loyal customers will be left in YouTube?

YouTube collected personal info on people who has been unloading videos on its site and has revealed ID to Paramount lawyers who sue the poor guy in the court:

http://www.boingboing.net/2006/10/23/youtube_gave_user_da.html

http://www.boingboing.net/2006/10/23/youtube_gave_user_da.html

How much upside is left even to Google's craziest valuation?

When will the game "music chairs" begin? Who will be without the place? In order to Sell you need to have a buyer. If you are buying Google at 480.78, you are buying the company with following valuation from Hard Data on Google Bear Case:

FCF 2006 est 1.712 billion

GAAP EPS 9.44 USD

Revenue 10.4 billion

Market cap at 480.78 stands for 149,3 billion. After YouTube deal if stock will not move from 480.78 dilution will be +3.4 million shares wich will bring Market Cap to 151 billion.

So at 480.78 Google is "on sale" according to majority of analysts with:

2006 est MC/FCF=88.2, P/E=50.9, P/S=14.5 with growth in Revenue in single digits Q/Q and EPS growth +1.3% Q3/Q2 in slowing economy with online advertisement slowing growth reality.

FCF 2006 est 1.712 billion

GAAP EPS 9.44 USD

Revenue 10.4 billion

Market cap at 480.78 stands for 149,3 billion. After YouTube deal if stock will not move from 480.78 dilution will be +3.4 million shares wich will bring Market Cap to 151 billion.

So at 480.78 Google is "on sale" according to majority of analysts with:

2006 est MC/FCF=88.2, P/E=50.9, P/S=14.5 with growth in Revenue in single digits Q/Q and EPS growth +1.3% Q3/Q2 in slowing economy with online advertisement slowing growth reality.

Monday, October 23, 2006

S&P DOWNGRADES CLASS A SHARES OF GOOGLE TO HOLD FROM BUY ON VALUATION

"S&P DOWNGRADES CLASS A SHARES OF GOOGLE TO HOLD FROM BUY ON VALUATIONS&P Marketscope - October 23, 2006 2:47 PM ETShares are up 19% this month, and are approaching our recently increased 12-month target price of $500. We remain positive on GOOG's fundamentals specifically, and online advertising in general. However, risk-reward considerations contribute significantly to our downgrade. With GOOG today reaching an all-time intra-day high, we are growing increasingly wary of what we perceive to be potentially excessive enthusiasm regarding the company and stock. At current levels, we see the shares as only reasonably valued. "

http://yahoo.reuters.com/news/articlehybrid.aspx?type=comktNews&storyID=urn:newsml:reuters.com:20061023:MTFH41903_2006-10-23_19-55-46_N23390483&pageNumber=1&imageid=&cap=&sz=13&WTModLoc=HybArt-C1-ArticlePage1

http://yahoo.reuters.com/news/articlehybrid.aspx?type=comktNews&storyID=urn:newsml:reuters.com:20061023:MTFH41903_2006-10-23_19-55-46_N23390483&pageNumber=1&imageid=&cap=&sz=13&WTModLoc=HybArt-C1-ArticlePage1

Some guys are still using their brains and calculators in Google case

As written here before Google's Revenue growth is slowing :

http://internet.seekingalpha.com/article/18996

http://internet.seekingalpha.com/article/18996

Is Google an Organizer or just Polluter of the WEB?

Very big academic debate will be held in the nearest future: was Google phenomenon good for development of the WEB or was it time of Rubber barons in the New Economy. It looks like that on every Conner of the WEB only Rubbish with parked pages could be found and you really have to start filtering all information which is coming from search engines.

Great read:

http://blogs.zdnet.com/micro-markets/?p=576

Great read:

http://blogs.zdnet.com/micro-markets/?p=576

Washington post "FBI, SEC and US Postal Inspection Service are investigating click fraud"

This is the real story behind all that industry denial:

"Big advertisers are pushing search engines behind the scenes to fight click fraud more aggressively, but many are afraid to criticize them publicly because they wield such clout. "Sixty percent of new customers come through Google. [Advertisers] can't afford to upset that channel, regardless of whether there's fraud," said Jason Clement, an associate director at Carat Fusion, a New York ad agency."

http://www.washingtonpost.com/wp-dyn/content/article/2006/10/21/AR2006102100936.html

Very interesting discussion on

http://battellemedia.com/archives/003003.php

"Big advertisers are pushing search engines behind the scenes to fight click fraud more aggressively, but many are afraid to criticize them publicly because they wield such clout. "Sixty percent of new customers come through Google. [Advertisers] can't afford to upset that channel, regardless of whether there's fraud," said Jason Clement, an associate director at Carat Fusion, a New York ad agency."

http://www.washingtonpost.com/wp-dyn/content/article/2006/10/21/AR2006102100936.html

Very interesting discussion on

http://battellemedia.com/archives/003003.php

Sunday, October 22, 2006

Google's growth is slowing dramatically

Few more observations on recent trends in Revenue and Net Margin of google presented in CC slides

First of all I dare to say that they have monetised everything from the existing traffic with diminishing growth and they are desperate to buy new traffic in order to monetise it. The biggest problem here that YouTube traffic is not monetisable straight forward if meaningfully monetisable at all. But few figures: Growth in Google.com is in the slowing trend Q3/05 +20%; Q4/05 +24%; Q1/06 +18%; Q2/06 +10.4%; Q3/06 +13.5%. Share of Network Revenue is declining Q2/05 85%; Q3/05 76.3%; Q4/05 72.8%; Q1/06 71.5%; Q2/06 69.6%; Q3/06 63.8% and growth in Network revenue is slowing even more aggressively: Q3/05 +7%; Q4/05 +18%; Q1/06 +16%; Q2/06 +7.4%; Q3/06 +4% (!) What has happen? Partners has figured out how to monetise traffic without Google? Nobody is growing apart from Google (which is slowing down itself)? Click fraud with better audit available to advertisers is taking its cut from "partners" clicks? We can only speculate here, but trend is established and it must be very disturbing to Google management. Cost of this Network traffic is increasing, if you will proper apply TAC to share of Network Revenue you can see following picture: TAC/NetwRev Q2/05 78.4%; Q3/05 60%; Q4/05 78.7%; Q1/06 77.9%; Q2/06 78.7%; Q3/06 79.6%. So total picture is that growth of Revenue on Google.com is slowing to 12-15%; Growth of Network Revenue is slowing dramatically to single digit figures and its cost TAC pushing 80%. Net Network Revenue was Q1/06 205 mil 15.8% of Rev Google.com; Q2/06 212 mil 14.8%; Q3/06 212 mil (!) 13%. Somebody is playing math here? Do you remember how insurance companies like AIG smoothed their earning with "Partner Deals"? Traffic exchange even more easy to regulate or maybe some of the "Partners" in the "Network" in the Family. But no offence Boys - you are hardly pushing any Law here and clear in your intentions: Selling your shares smooth and fast. All written above went straight into the money: Net margin contracted in Q3 vs Q2 from 29.4% to 27.3%. Should I send it to Google? Or they already have these slides for internal use?

Saturday, October 21, 2006

Google just 460...Anyone?

It was not a lot of institutional buyers at 460 last Friday:

http://thomson.finance.lycos.com/lycos/iwatch/cgi-bin/iw_ticker?ticker=goog

Coming week will be very interesting with all markets at crossroads, I will post few charts for Lazy weekend session.

Almost everybody thinks that Fed is Done but what if More Fed's hikes are coming:

http://money.cnn.com/2006/10/19/news/economy/inflation/index.htm?source=yahoo_quote

Good weekend educational read:

http://financialsense.com/

http://jsmineset.com/

http://gold-eagle.com/

http://prudentbear.com/

When you are tired:

http://www.valleywag.com/tech/google/

Google CC:

http://internet.seekingalpha.com/article/18858

http://thomson.finance.lycos.com/lycos/iwatch/cgi-bin/iw_ticker?ticker=goog

Coming week will be very interesting with all markets at crossroads, I will post few charts for Lazy weekend session.

Almost everybody thinks that Fed is Done but what if More Fed's hikes are coming:

http://money.cnn.com/2006/10/19/news/economy/inflation/index.htm?source=yahoo_quote

Good weekend educational read:

http://financialsense.com/

http://jsmineset.com/

http://gold-eagle.com/

http://prudentbear.com/

When you are tired:

http://www.valleywag.com/tech/google/

Google CC:

http://internet.seekingalpha.com/article/18858

Hard Data on Google Bear Case

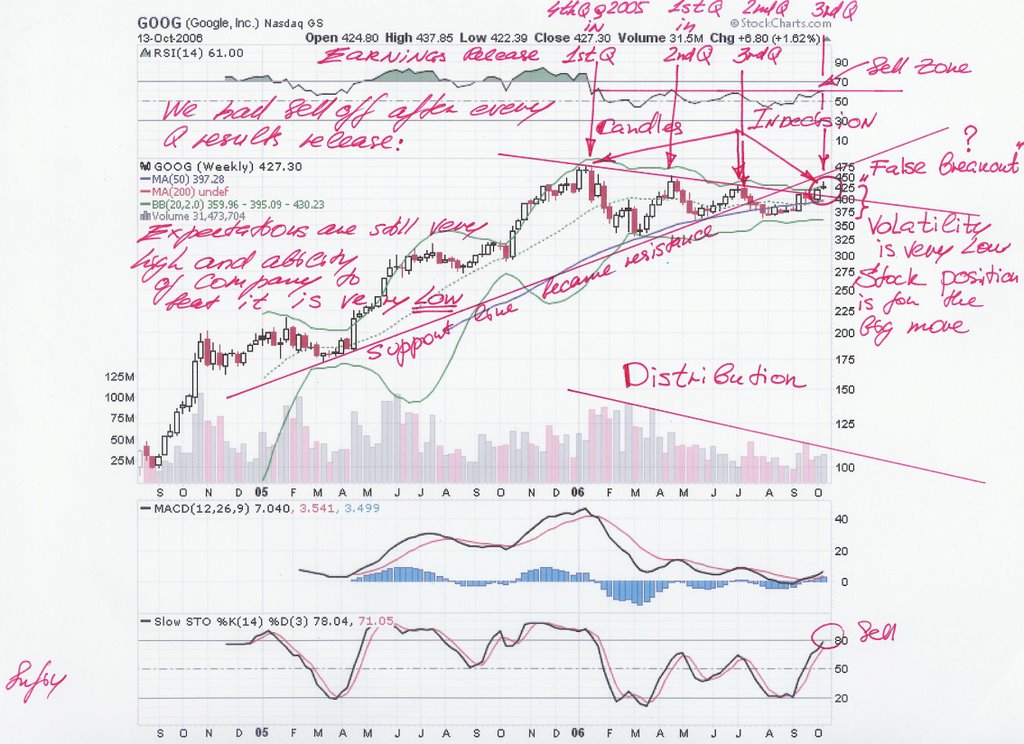

Lets keep all media hype away and quick short covering amusement following it and check out Google's development in recent Q in order to try to understand its valuation compare to its piers. Upside now is known and everybody is on Buy side with price target 600 (+30%). Shorts are killed and short ratio is less than one day trade, no easy money for upside after yestoday short covering left, somebody has to start to buy into this story at this 460 level. First Google came with Rev 2.69 billion which is less then 2.76 which I have projected from PWC predictions of 16-18 billion online ads market in 2006 with Google Share of 40.5% of this market in Q3 (seasonal trend applied) So, first Google did not manage to increase its market share in Q3. Second, lets look at earnings GAAP ($) Q1 1.95, Q2 2.33 (+19%), Q3 2.36 (+1.3%!?) Earnings growth dramatically slowed. Third, revenues: Q1 2.25, Q2 2.46 (+9.3%), Q3 2.69 (+9.3%!?) math's precision or can I smell some cooking oil here? 44% of revenue is coming from international business. All hitfarms are located in pure "international "destinations India, China, Malaysia, Russia etc. Revenue growth is slowing with increased risk of cutting back on advertisement due to economy slowdown and click fraud awareness buy the customers. Fourth, Net cash from operations Q1 0.825 (37% of Rev), Q2 0.841 (+2% 34% of Rev), Q3 1.0 (+19% 37% of Rev) Capex Q2 0.699 (0.319 Real eastate 0.380 "normalised"), Q3 0.492 (+29%!) So Google Capex increase is really much bigger then their Rev growth 29% vs 9.3% with constant Net cash from operations at 37% Rev, Free Cash Flow is under compression. Total Free Cash Flow for nine months is 1.112. If we will project Rev growth for Google at 12% for Q4 vs 9.3% for Q3 they will make Rev Q4 3.0 (less then based on PWC and 41% of market 3.2) Net cash from operations at 37% of Rev 3.0 will be 1.1, if we apply 20% growth for NCFO in Q4 (vs +19% Q3) we will get 1.2 so lets assume NCFO will be in the middle = 1.15. What about Capex? I think it will be increasing dramatically with moving into video: broadband, storage, new blades, electricity. But if we even aply same growth to capex as to Rev +12% (they said it will be bigger then Rev growth, Q3 was +29%) Capex Q4 will be 0.551. So, Free Cash Flow in Q4 will be NCFO-CAPEX=0.6 and total FCF 2006 will be 1.712 If stock will not move from 460 we have MC=142 billion MC/FCF=83! YHOO is projecting FCF 1.35 in 2006 (lowered recently) with MC at 32 their ratio is MC/FCF=24 If the Google will manage to make even 2.8 EPS in Q4 (+19%) (do not forget annual charge for all those "to be expenced option related expences which they did not account in past Qs) GAAP 2006 will be 9.44. So with GOOG at 460 we have company with 2006 est MC/FCF=83, P/E=48.7, P/S=14.2 with slowing growth in EPS and Revenue and most important with dramatic compression in FCF. YouTube will bring dilution, much more CAPEX in Video Game and No revenue so far. What is the more reasonable valuation of Google: if we give GOOG MC/FCF=40 (69% over YHOO for leadership and "strength") MC with 1.712 FCF must be 68.5 billion with 310 million shares outstanding before YouTube diluton it is...221 share price. When MR Market will figure it out I do not know, but I am testing the water with March 2007 460 puts.

Friday, October 20, 2006

Reflection...time to think it over. CS

Ok, GOOG at 460, it is time for reflection. First I must admit: ability of this company to create perception in the market that they have beat every possible estimation and move the share price higher is unmatchable, or here I am wrong – guys from YouTube maybe even better, and it is great for them if they will sell shares of GOOG in due time. But admission to be made: GOOG have broken to the upside on earnings from triangle on weekly bases. I was wrong here and predicted that it will be breaking down. So we must study the facts, check the strategy and move on. When I would be completely wrong: if I have put all my short position on this earnings without any limit of risk, so few rules to stay in this game until the end of education:

Allow at least twice as much time for your thesis to be developed in the market as you can anticipate in the beginning.

It is still very difficult: you have some help: Roll Over your position.

If you Trade then close position as soon as you have profit that you have anticipated in the beginning and take you capital out, let you profit run If thesis still in place.

How to stay in the game: Trade only with money which you could afford to lose: limit your risk by buying PUTs on stocks which you think are overvalued.

So what is my case: I am Investor in big long term trend: now it is commodities, PGM, Silver, Uranium, alternative energy. All my major positions are there: I am using TA to reduce my positions on the tops and to increase them in the bottoms. Here my horizon is years. I am buying value in undeveloped resources – mining companies: it is like option trade on the underlying commodity but without time value to lose. Not Risky? No way, but I had very expensive education and now is doing good job. Am I as good as I am writing now – this is the whole point of this Blog: I can be way better, particularly in Trade. So this is part of my education: I have allocated some capital on ongoing bases and trying to bring my skills to perfection, here where the Google comes: I really like technology and using it everywhere and Google as well and Blogger (maybe because I am PC illiterate). But when we talk about Google Company valuation it is another story.

Probably, according to research and massive comments I am the only reader of this Blog – better for me: Warren Buffet will not compete with my positions. And I do not like that Larry and Sergey after reading it will change their strategy and will buy all Junior mining companies with their shares: they are already wealthy, actually without knowing me are doing the same (only selling shares of GOOGLE, it is very strange that they are not buying it like crazy with guaranteed upside to 600) and my turn to make a lot of money on Irrational Exeburation in WEB BUUBLE 2.0 is still to come. Sorry I can not disclose my Junior mining trades apart from already posted information: their market caps are so small that it takes me months to establish proper positions. But leave me a comment and for the good devoted to thinking guys and girls there is nothing to be jealous about.

So talking about business I will post my take on earnings and why I am not buying calls but rather puts March 07 and further down the road. Why to bother? Another Rule:

Never marry your position, do not bring your trade or even investment to Personal level: if the thesis changed close the Trade and move on.

From personal experience: If you are healthy and have capital, another idea and opportunity will find you, in different case nobody will call.

What I did well this year in trading: Puts on GM, YHOO, INTC, QQQQ, KBH, LEN, TOL, DIA, AAPL all closed with profit. Now new are established PUT QQQQ, SMH, DIA, SNDK, NVDA, RIMM. Warrants on NNO, GG closed with profit. Now calls are established on SSRI, SLW, GG, RGLD. Google PUT closed with profit in May – June and Rolled Over into Jan 07 (bought new positions Long Put with longer term of Expiration). Am I perfect and satisfied, no - I could do better particularly with GOOG, RIMM and expect that more time will be needed until Irrational Exuberance will be apparent to the market and take into account that some Saudi friends can help someone with elections bringing oil down and effectively markets up. Thanks them for it: I had good Juniors Hunting recently. Few more streaming thoughts before Bear GOOGLE Hard Data thesis posted: today I have closed very nice Trade on SNDK: it was down 21% and my PUTs were flying: very perfect education case. I enter small position in the beginning of the year too early and too out of the money (after today drop even there I can break even), but let myself test the water, on recent spike I have established proper position and today thesis was developed by the market, valuation PERCEPTION was changed and stock was beaten HARD so I ended with nice profit. Why SNDK fall? They beat the Street 0.51 vs 0.49 and on revenue 2% above Street est. but they guided lower! And everybody sell them, GOOG keep silence about the outlook and the same guys who punish SNDK with $46 PT are putting on GOOG PT of $595. Look at their fundamentals in the same report: SNDK forward P/E 2006 is 30.1 est. and 2007 is 28.7 GOOG frwd P/E 2006 is 41.8 and 2007 is 30.4. One stock is down 21% and another is up 7.5%. Here comes another very important issue: PERCEPTION and it could cost you all your money you can be THOUSAND times right, but if perception of the MR Market has not agreed with you, you can lose everything and in options TIME which is against you when you are long options is most crucial factor: Google can go into oblivion in 5 years but if you had Oct 2006 400 puts you Capital will not make it. That is why (according to open sources) Warren Buffet is never playing options, he is …”just not clever enough” as he puts it. One thing is to find out right direction another is to figure out the timeframe when that direction will be realised. Am I trying to be clever than him? Nope, just “sharping the saw”. At the moment bad story about SNDK is known, with GOOGLE with WORSE fundamentals perception is that everything is growing fast and upside is unlimited. What is very important with SNDK: there is no pricing power, competition in COMMODITY business (search is UNIQUE and RESTRICTED to Google?), lower sales (I bet due to Consumer hurt by Housing Bubble bursting and cut back of all users of SNDK on Inventory levels due to Not Rosy outlook) will they cut on chips but spend on ADs even more – hardly and we can see it already in Google financials). Before Hard Data just take a look on Rev growth q on q this q3 it was 9.3% not 10% in conference call (are they pushing figures only here?) but in q2 on q1 Rev Growth was … the same 9.3% miracle, or can I smell some cooking oil? Then we can find out that international Rev contributed 44%, where from do you think click fraud originated: China, Malaysia, Russia and other “pure international destinations”. Why do they use Non GAAP figures together with GAAP ones just for confusion, they love Buffet but he never do it. Why is there is always mysterious:

“Stock-Based Compensation – In the third quarter, the total charge related to stock-based compensation was $100 million as compared to $109 million in the second quarter.

For the full year, we expect stock-based compensation charges for grants to employees prior to October 1, 2006 to be $377 million. This does not include expenses to be recognized over the remainder of the year related to employee stock awards that are granted after October 1, 2006 or non-employee stock awards that have been or may be granted. We currently anticipate that dilution related to all equity grants to employees will be approximately 1% to 1.5% per year.”

Why do not expense all related to the q costs of Labour in all categories of compensation? The only reason that you can play with it but at the year end you will have to charge it. But more to come in hard data posting.

Few final disclosures: because if you Think you will always ask Who? What? And Why? I am not so old; my background is in Finance with applications in telecom, transportation, banking, and internet. Mining and PGM lately, strategic controlling in fast developing Holding of companies in different industries in emerging markets was my last managerial application. Now I have a treasure to Think, Act and Enjoy accordingly. I do not believe in Efficient Market - otherwise I can not afford my lifestyle. Why? I am not sure, definitely for myself and my son and maybe few others…If I will stop posting it means that I have figured out more efficient way of keeping myself to the account. English is not my native, sorry. Sufiy…it is very special and I am not Muslim (nothing wrong with it anyway). Always remember there are a lot of PhDs in the world, but not everyone of them is a millionaire. You need something else, I would rather call it Art. (I am not PhD)

http://investor.google.com/releases/2006Q3.html

Allow at least twice as much time for your thesis to be developed in the market as you can anticipate in the beginning.

It is still very difficult: you have some help: Roll Over your position.

If you Trade then close position as soon as you have profit that you have anticipated in the beginning and take you capital out, let you profit run If thesis still in place.

How to stay in the game: Trade only with money which you could afford to lose: limit your risk by buying PUTs on stocks which you think are overvalued.

So what is my case: I am Investor in big long term trend: now it is commodities, PGM, Silver, Uranium, alternative energy. All my major positions are there: I am using TA to reduce my positions on the tops and to increase them in the bottoms. Here my horizon is years. I am buying value in undeveloped resources – mining companies: it is like option trade on the underlying commodity but without time value to lose. Not Risky? No way, but I had very expensive education and now is doing good job. Am I as good as I am writing now – this is the whole point of this Blog: I can be way better, particularly in Trade. So this is part of my education: I have allocated some capital on ongoing bases and trying to bring my skills to perfection, here where the Google comes: I really like technology and using it everywhere and Google as well and Blogger (maybe because I am PC illiterate). But when we talk about Google Company valuation it is another story.

Probably, according to research and massive comments I am the only reader of this Blog – better for me: Warren Buffet will not compete with my positions. And I do not like that Larry and Sergey after reading it will change their strategy and will buy all Junior mining companies with their shares: they are already wealthy, actually without knowing me are doing the same (only selling shares of GOOGLE, it is very strange that they are not buying it like crazy with guaranteed upside to 600) and my turn to make a lot of money on Irrational Exeburation in WEB BUUBLE 2.0 is still to come. Sorry I can not disclose my Junior mining trades apart from already posted information: their market caps are so small that it takes me months to establish proper positions. But leave me a comment and for the good devoted to thinking guys and girls there is nothing to be jealous about.

So talking about business I will post my take on earnings and why I am not buying calls but rather puts March 07 and further down the road. Why to bother? Another Rule:

Never marry your position, do not bring your trade or even investment to Personal level: if the thesis changed close the Trade and move on.

From personal experience: If you are healthy and have capital, another idea and opportunity will find you, in different case nobody will call.

What I did well this year in trading: Puts on GM, YHOO, INTC, QQQQ, KBH, LEN, TOL, DIA, AAPL all closed with profit. Now new are established PUT QQQQ, SMH, DIA, SNDK, NVDA, RIMM. Warrants on NNO, GG closed with profit. Now calls are established on SSRI, SLW, GG, RGLD. Google PUT closed with profit in May – June and Rolled Over into Jan 07 (bought new positions Long Put with longer term of Expiration). Am I perfect and satisfied, no - I could do better particularly with GOOG, RIMM and expect that more time will be needed until Irrational Exuberance will be apparent to the market and take into account that some Saudi friends can help someone with elections bringing oil down and effectively markets up. Thanks them for it: I had good Juniors Hunting recently. Few more streaming thoughts before Bear GOOGLE Hard Data thesis posted: today I have closed very nice Trade on SNDK: it was down 21% and my PUTs were flying: very perfect education case. I enter small position in the beginning of the year too early and too out of the money (after today drop even there I can break even), but let myself test the water, on recent spike I have established proper position and today thesis was developed by the market, valuation PERCEPTION was changed and stock was beaten HARD so I ended with nice profit. Why SNDK fall? They beat the Street 0.51 vs 0.49 and on revenue 2% above Street est. but they guided lower! And everybody sell them, GOOG keep silence about the outlook and the same guys who punish SNDK with $46 PT are putting on GOOG PT of $595. Look at their fundamentals in the same report: SNDK forward P/E 2006 is 30.1 est. and 2007 is 28.7 GOOG frwd P/E 2006 is 41.8 and 2007 is 30.4. One stock is down 21% and another is up 7.5%. Here comes another very important issue: PERCEPTION and it could cost you all your money you can be THOUSAND times right, but if perception of the MR Market has not agreed with you, you can lose everything and in options TIME which is against you when you are long options is most crucial factor: Google can go into oblivion in 5 years but if you had Oct 2006 400 puts you Capital will not make it. That is why (according to open sources) Warren Buffet is never playing options, he is …”just not clever enough” as he puts it. One thing is to find out right direction another is to figure out the timeframe when that direction will be realised. Am I trying to be clever than him? Nope, just “sharping the saw”. At the moment bad story about SNDK is known, with GOOGLE with WORSE fundamentals perception is that everything is growing fast and upside is unlimited. What is very important with SNDK: there is no pricing power, competition in COMMODITY business (search is UNIQUE and RESTRICTED to Google?), lower sales (I bet due to Consumer hurt by Housing Bubble bursting and cut back of all users of SNDK on Inventory levels due to Not Rosy outlook) will they cut on chips but spend on ADs even more – hardly and we can see it already in Google financials). Before Hard Data just take a look on Rev growth q on q this q3 it was 9.3% not 10% in conference call (are they pushing figures only here?) but in q2 on q1 Rev Growth was … the same 9.3% miracle, or can I smell some cooking oil? Then we can find out that international Rev contributed 44%, where from do you think click fraud originated: China, Malaysia, Russia and other “pure international destinations”. Why do they use Non GAAP figures together with GAAP ones just for confusion, they love Buffet but he never do it. Why is there is always mysterious:

“Stock-Based Compensation – In the third quarter, the total charge related to stock-based compensation was $100 million as compared to $109 million in the second quarter.

For the full year, we expect stock-based compensation charges for grants to employees prior to October 1, 2006 to be $377 million. This does not include expenses to be recognized over the remainder of the year related to employee stock awards that are granted after October 1, 2006 or non-employee stock awards that have been or may be granted. We currently anticipate that dilution related to all equity grants to employees will be approximately 1% to 1.5% per year.”

Why do not expense all related to the q costs of Labour in all categories of compensation? The only reason that you can play with it but at the year end you will have to charge it. But more to come in hard data posting.

Few final disclosures: because if you Think you will always ask Who? What? And Why? I am not so old; my background is in Finance with applications in telecom, transportation, banking, and internet. Mining and PGM lately, strategic controlling in fast developing Holding of companies in different industries in emerging markets was my last managerial application. Now I have a treasure to Think, Act and Enjoy accordingly. I do not believe in Efficient Market - otherwise I can not afford my lifestyle. Why? I am not sure, definitely for myself and my son and maybe few others…If I will stop posting it means that I have figured out more efficient way of keeping myself to the account. English is not my native, sorry. Sufiy…it is very special and I am not Muslim (nothing wrong with it anyway). Always remember there are a lot of PhDs in the world, but not everyone of them is a millionaire. You need something else, I would rather call it Art. (I am not PhD)

http://investor.google.com/releases/2006Q3.html

Saturday, October 14, 2006

Wednesday, October 11, 2006

More news on slowing advertisement

"CNet also lowered its revenue outlook for the third quarter, citing weaker-than-expected advertising demand. The company now expects revenue of $92.8 million, below its previous forecast of $93 million to $96 million.

Also, CNet lowered its 2006 revenue project to $376 million to $386 million from the previously stated $386 million"

Tuesday, October 10, 2006

WEB 2.0 turns into BUBBLE 2.0 Google buys YouTube

On this deal WEB 2.0 has turned into bubble 2.0. Google has admitted that inside nothing substantial could be created, the main logic was "if we will not buy it MSFT or AHOO will! And then what...Google will vanish? Where is all that brand strength, dominant market share? The truth is it is one stream revenue business, competitors just ONE CLICK away, cost switch for customer Zero. Look at their CC about the deal: company is under hit of contracting revenue growth and most importantly FCF, which will bring valuation and stock price down. The most interesting for me is how they are going make this q, numbers are gonna be very thought to meet.

Please note that in my EPS estimation below I have used all current trends in spending but revenue growth is +12.5% Q3/Q2 and +17%(!) Q4/Q3 they manage to make only +9% on Q2/Q1.

Please note that in my EPS estimation below I have used all current trends in spending but revenue growth is +12.5% Q3/Q2 and +17%(!) Q4/Q3 they manage to make only +9% on Q2/Q1.

Sunday, October 08, 2006

Weekend lazy: food for thoughts on recent trends...

Mixed outlook for advertisement

http://www.ft.com/cms/s/f55f202e-4cbf-11db-b03c-0000779e2340.html

Online video is not a priority

http://www.adweek.com/aw/national/article_display.jsp?vnu_content_id=1003189673

Online advertising slows:

http://money.cnn.com/2000/10/05/redherring/herring_online/

Options is not good motivation at GOOGLE any more! Executives prefers hard cash, it is very strange I thought GOOG at 600 will be better:

http://www.redherring.com/Article.aspx?a=19015&hed=Have+Google+Options+Lost+Luster%3f

US Online Ad Spending:Peak or Plateau?

http://www.emarketer.com/Reports/All/Em_ad_spend_oct06.aspx

PWC report

http://www.iab.net/resources/adrevenue/pdf/IAB_PwC%202006Q2.pdf

http://www.ft.com/cms/s/f55f202e-4cbf-11db-b03c-0000779e2340.html

Online video is not a priority

http://www.adweek.com/aw/national/article_display.jsp?vnu_content_id=1003189673

Online advertising slows:

http://money.cnn.com/2000/10/05/redherring/herring_online/

Options is not good motivation at GOOGLE any more! Executives prefers hard cash, it is very strange I thought GOOG at 600 will be better:

http://www.redherring.com/Article.aspx?a=19015&hed=Have+Google+Options+Lost+Luster%3f

US Online Ad Spending:Peak or Plateau?

http://www.emarketer.com/Reports/All/Em_ad_spend_oct06.aspx

PWC report

http://www.iab.net/resources/adrevenue/pdf/IAB_PwC%202006Q2.pdf

How online gambling collapse will affect online advertisement

It will be very interesting to get estimation how Google, Yahoo and internet advertisers were affected generally by collapse of online gaming companies:

http://www.theherald.co.uk/business/71399.html

http://www.google.com/trends?q=online+gaming%2C+online+casino%2C+online+pocker&ctab=0&geo=US&date=all

http://www.theherald.co.uk/business/71399.html

http://www.google.com/trends?q=online+gaming%2C+online+casino%2C+online+pocker&ctab=0&geo=US&date=all

Saturday, October 07, 2006

It was not sobering: it is desperation - Google in talks to buy YouTube!

From Henry Blodget:

http://www.internetoutsider.com/google/index.html

Sorry Henry, If I can disagree here: I can see this move of Google to buy YouTube as act of desperation to diversify from one stream revenue business which is slowing down with click fraud and slowing economy on one side and finally sobering thoughts of founders on all crap products they announced which are not working and/or not wanted by anyone on another. I can imaging that after a big battle inside and clear understanding that all very expensive R&D are not bringing NEW PRODUCTS WHICH ARE ADDING to revenue and bottom line they were pushed to make a move which suppose to bring new dimension and advertisement space for monetisation efforts. Will it save GOOGLE from falling short of expectations – I doubt it. Apart from copyright issues fully described by Mark Cuban and others from business point of view this acquisition is wrong at the wrong point in time: YouTube is just a place where people are unloading their video content - it is real “LONG TAIL” staff, 99% of it will be seen just by creator and five other guys maximum. In order to monetise this audience media it will take ages and maybe never be profitable. If I would like to see news I will go to news portal, I will use good video search engine for lectures or similar CONTENT. Apart from hype this 1.6 billion investment will not bring any even middle term (1-3 years) google size meaningful revenues. So we have now very interesting point of Google business development cycle which will be reflected in earnings this and next quarter: no new working ideas from inside, all released products are not material in sense of revenue, strategy is to move into video space and buy out time but there is no clear business idea apart from proposal to advertisers: now we will put your add on every video download (99% is how I am cool dancing or baking or nice place in Zumbaramba). On the margin compression side we will have slowing growth of revenue due to click fraud recognition and slowing economy (not only YAHOO! disease), increasing Capex (now with not clear picture whether any of these investments are actually working) and expense related to options from 1st and 2nd q around 151 mil, so Free Cash Flow will be way below to reflect any sustainable multiple to the current stock price.

http://www.internetoutsider.com/google/index.html

Sorry Henry, If I can disagree here: I can see this move of Google to buy YouTube as act of desperation to diversify from one stream revenue business which is slowing down with click fraud and slowing economy on one side and finally sobering thoughts of founders on all crap products they announced which are not working and/or not wanted by anyone on another. I can imaging that after a big battle inside and clear understanding that all very expensive R&D are not bringing NEW PRODUCTS WHICH ARE ADDING to revenue and bottom line they were pushed to make a move which suppose to bring new dimension and advertisement space for monetisation efforts. Will it save GOOGLE from falling short of expectations – I doubt it. Apart from copyright issues fully described by Mark Cuban and others from business point of view this acquisition is wrong at the wrong point in time: YouTube is just a place where people are unloading their video content - it is real “LONG TAIL” staff, 99% of it will be seen just by creator and five other guys maximum. In order to monetise this audience media it will take ages and maybe never be profitable. If I would like to see news I will go to news portal, I will use good video search engine for lectures or similar CONTENT. Apart from hype this 1.6 billion investment will not bring any even middle term (1-3 years) google size meaningful revenues. So we have now very interesting point of Google business development cycle which will be reflected in earnings this and next quarter: no new working ideas from inside, all released products are not material in sense of revenue, strategy is to move into video space and buy out time but there is no clear business idea apart from proposal to advertisers: now we will put your add on every video download (99% is how I am cool dancing or baking or nice place in Zumbaramba). On the margin compression side we will have slowing growth of revenue due to click fraud recognition and slowing economy (not only YAHOO! disease), increasing Capex (now with not clear picture whether any of these investments are actually working) and expense related to options from 1st and 2nd q around 151 mil, so Free Cash Flow will be way below to reflect any sustainable multiple to the current stock price.

Friday, October 06, 2006

Looks like sobering thoughts for me

Finally from Google founders: this kind of unsustainable and irresponsible financially CAPEX investments into the products which do not work and do not wanted is very precise indicator of BUBBLE ready to burst.

What developments have turned unstoppable we-will-fix-everything guys to more sober state of minds? Slowing monetisation efforts, ADs cut back due to click fraud and economy slow down or just common sense? This earnings release will be very interesting!

"Google (GOOG) leaders told their engineers to stop focusing on launching a dizzying array of new services, and concentrate on making sure the existing ones work. "I was getting lost in the sheer volume of the products we were releasing," said co-founder Sergey Brin. The Internet search giant's Web sites offer more than 50 products in various stages of development, from digital maps to a search engine for mail-order catalogs. "They created a bunch of crap that they have no idea what to do with," said Rob Enderle, principal analyst of the Enderle Group. (Los Angeles Times, free registration required)"

http://finance.yahoo.com/columnist/article/business/10534

What developments have turned unstoppable we-will-fix-everything guys to more sober state of minds? Slowing monetisation efforts, ADs cut back due to click fraud and economy slow down or just common sense? This earnings release will be very interesting!

"Google (GOOG) leaders told their engineers to stop focusing on launching a dizzying array of new services, and concentrate on making sure the existing ones work. "I was getting lost in the sheer volume of the products we were releasing," said co-founder Sergey Brin. The Internet search giant's Web sites offer more than 50 products in various stages of development, from digital maps to a search engine for mail-order catalogs. "They created a bunch of crap that they have no idea what to do with," said Rob Enderle, principal analyst of the Enderle Group. (Los Angeles Times, free registration required)"

http://finance.yahoo.com/columnist/article/business/10534

Wednesday, October 04, 2006

Tuesday, October 03, 2006

Monday, October 02, 2006

{kind=link}

Subscribe to:

Posts (Atom)