Frank Holmes presents a very interesting set of charts supporting the bullish case for Gold and Gold stocks. Now with Gold crossing 200MA we have the game changer for the Gold marker. Professional traders have positioned themselves after 20MA was breaking out to the upside and smart money has followed after 50MA. Now the retail public will start buying the new Gold Bull leg.

Number of Gold stocks with, McEwen Mining among them, has printed The Golden Cross already, when 50MA is crossing 200MA to the upside, confirming the bullish reversal pattern. It is very bullish set up and we expect the rally in Gold stocks to widen its base to include the smaller junior miners.

TNR Gold TNR.V is one of the most intriguing microcap stories I follow.#insidersbuying cc:@Sufiy@TedDixon@inkresearch

Gold Breaks 1,320: The Mother Of Short Squeeze Has Arrived TNR.v MUX GDX GLD SLV RGLD ABX GG

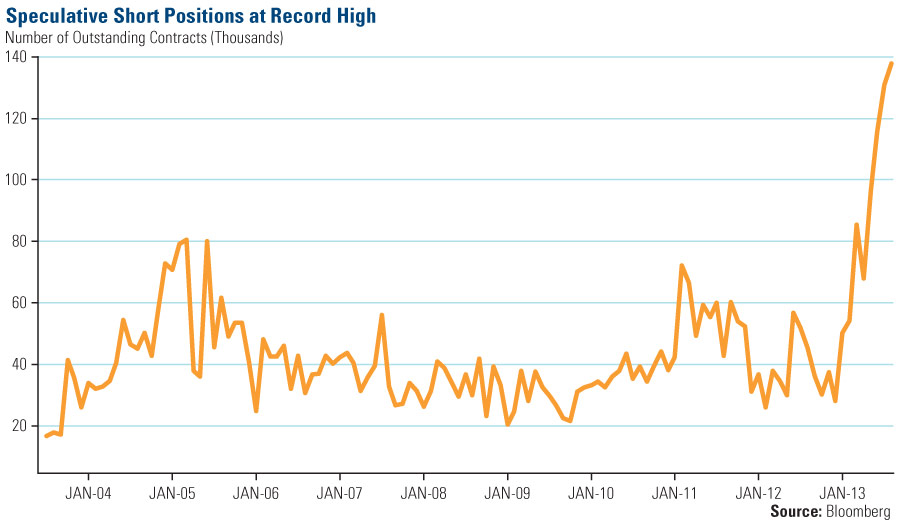

"Gold is sending its Happy Valentines to all Gold Bugs today and breaks $1320 on the massive short squeeze. Gold shorts will have their Blood Friday now. The real reason for this move is the realisation of the groundbreaking shift in the structure of the Gold market with the unprecedented demand of 2,181 tons of Gold from China in 2013. Janet Yellen testimony has opened the possibility To Taper The Taper andJames Rickards is calling for the Taper Pause in June. US dollar is going down very close to 80.00 level again. This level will be protected, but should the US Dollar break down below 80.00 Gold and Silver will go vertical towards $1,500 and $25 respectively.Our short Squeeze watch includes McEwen Mining and TNR Gold. McEwen Mining had 26.8 million shares sold short or 8.6 days to cover, according to NASDAQ. MUX.to has rocketed from December low of CAD1.80 to CAD3.27 close yesterday. Gold breakout will push shorts into the corner, but explosive move in Silver will have even more effect on this company. TNR Gold is still day dreaming, but move in McEwen Mining should pull out this junior out of its misery. Los Azules Copper development will be next to watch on the back of recent M&A activity in the sector and CRB - commodity index breakout to the upside."

Frank Holmes:

These Gold Charts Will Make Your Heart Beat Faster

Gold lovers’ hearts beat faster last week, as the metal rose above $1,300 an ounce for the first time since November. The precious metal also climbed above its 200-day moving average, which hasn’t happened in about a year.

ISI’s John Mendelson noted that the generic gold future “rallied off its mid-December low and has decisively broken out above its downtrend line connecting the descending tops from late August, a near-term positive.” The next price he’s targeting is $1,350, the price gold was at in late October.

So while gold may correct over the next several months as the metal enters its seasonally weak period of the year, this looks promising for gold investors.

Here are a few more gold charts that just might have your heart beating faster:

1. The Love Trade Endures in the East

In January, 246 tons of gold were withdrawn from the Shanghai Gold Exchange, as China continues expressing its love for the precious metal. This marks a record level of gold deliveries on the exchange as well as a significant increase over the same time last year.

In January, 246 tons of gold were withdrawn from the Shanghai Gold Exchange, as China continues expressing its love for the precious metal. This marks a record level of gold deliveries on the exchange as well as a significant increase over the same time last year.

In addition, you can see on the chart below that January’s total also exceeds world mining production for the month.

As Ralph Aldis likes to say, “Once the metal moves from the West and goes into China, we won’t get that gold back very easily.”

As Ralph Aldis likes to say, “Once the metal moves from the West and goes into China, we won’t get that gold back very easily.”

2. Money Supply Grew Faster in January

In the first month of 2014, the M2 money supply, which is a measure of money supply that includes cash, savings and checking deposits, grew faster than the previous two years. In 2012, M2 grew 7.6 percent and in 2013, money supply rose 4.7 percent; at an annualized rate, January’s money supply growth “reached an annualized rate of increase of 8.75 percent,” according to Bloomberg’s Precious Metal Mining team.

In the first month of 2014, the M2 money supply, which is a measure of money supply that includes cash, savings and checking deposits, grew faster than the previous two years. In 2012, M2 grew 7.6 percent and in 2013, money supply rose 4.7 percent; at an annualized rate, January’s money supply growth “reached an annualized rate of increase of 8.75 percent,” according to Bloomberg’s Precious Metal Mining team.

This may mean “the U.S. Federal Reserve is trying to resurrect inflation, thus increasing the appeal of gold, the supply of which can only increase about 1.5 percent to 2.5 percent annually,” says Bloomberg.

Last year, gold started to take it on the chin when the real rate of return went from a negative 0.62 percent in March to a positive 0.54 percent by December. Like I told Jim Goddard from HoweStreet, a positive real rate of return is typically a major headwind for gold.

Last year, gold started to take it on the chin when the real rate of return went from a negative 0.62 percent in March to a positive 0.54 percent by December. Like I told Jim Goddard from HoweStreet, a positive real rate of return is typically a major headwind for gold.

Between March and December of 2013, two things happened: 1) Yields rose in anticipation that the Federal Reserve would begin tapering its bond purchases, and 2) the consumer price index declined. However, going forward, I anticipate that CPI will increase, and, given the modest economic growth we’ve been seeing in the U.S. economy, interest rates won’t be able to rise too quickly.

3. Gold Stocks Poised to Rebound After Rare 3-Year Loss

What I think is tremendously powerful for gold stock investors is this chart. At the beginning of January, we took a look back at the annual returns for the Philadelphia Gold & Silver Index. In three decades, there were only three times that gold stocks only saw a consecutive 3-year loss.

What I think is tremendously powerful for gold stock investors is this chart. At the beginning of January, we took a look back at the annual returns for the Philadelphia Gold & Silver Index. In three decades, there were only three times that gold stocks only saw a consecutive 3-year loss.

These aren’t the only gold charts to love. See more in my latest presentation from the World Money Show.

These aren’t the only gold charts to love. See more in my latest presentation from the World Money Show.

India’s demand for gold during the second quarter of 2013 topped all other countries, according to the latest World Gold Council data. As noted by GoldCore, the demand for gold in India rose to its “highest in the last 10 years,” with jewelry, bars and coins demand, capping 310 tons during the period.

India’s demand for gold during the second quarter of 2013 topped all other countries, according to the latest World Gold Council data. As noted by GoldCore, the demand for gold in India rose to its “highest in the last 10 years,” with jewelry, bars and coins demand, capping 310 tons during the period.